Snowflake Stock Climbs After Q2, Here’s What Investors Should Know

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

Snowflake (SNOW) has once again delivered strong growth, following up on a solid first quarter with another impressive set of results. The company’s latest earnings release gave investors plenty to cheer about, sending shares surging nearly 18% in morning trading.

Even with broader economic uncertainty weighing on the software companies, Snowflake continues to show strong resilience. Demand for its products is growing, and its customer base is expanding. Moreover, its growing focus on artificial intelligence (AI) is accelerating product adoption and growth.

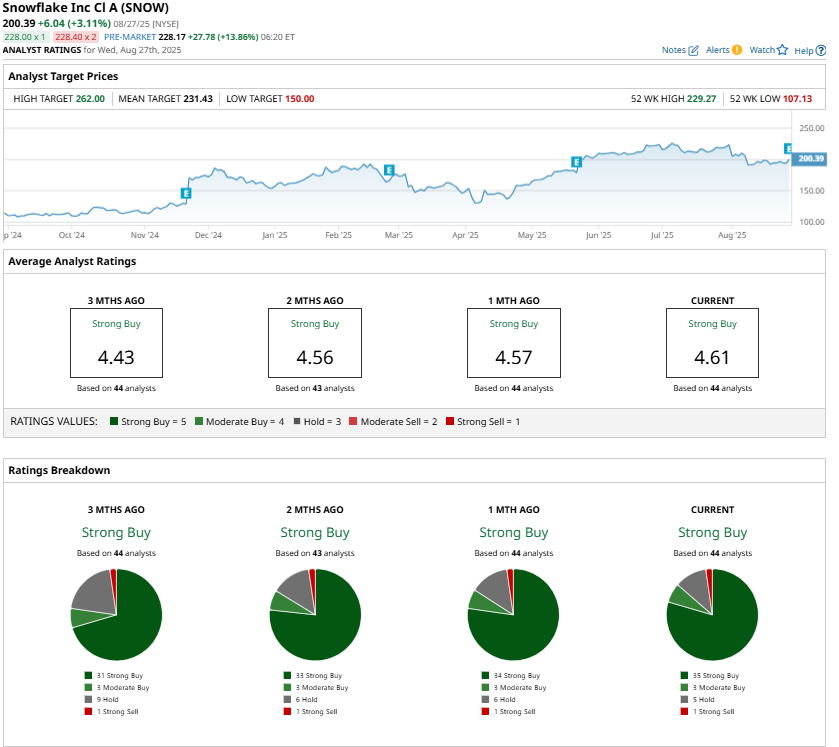

Adding to the optimism, management raised its full-year outlook once again. This upward revision reflects both the strength of Snowflake’s underlying business model and the vast market opportunity it is pursuing. The company’s large addressable market and strong backlog, reflected in its remaining performance obligations, highlight the durability of demand. These strengths have kept Wall Street analysts bullish, and the highest price target suggests that SNOW stock still has room to climb from its current price.

Snowflake Solid Growth Across Key Metrics

Snowflake’s core business remains solid, providing a strong foundation for future growth. By focusing on operational efficiency, Snowflake is strengthening profitability and freeing up resources to reinvest aggressively in new opportunities. This strength is reflected in its Q2 performance.

Snowflake’s latest quarterly results highlight both resilience and accelerating growth. The company reported product revenue of $1.09 billion for the second quarter, representing a 32% year-over-year increase. This marks a notable acceleration from the 26% growth seen in the previous quarter, reflecting the strong momentum in its core offerings.

Notably, demand was broad-based, with new features across multiple product categories exceeding expectations. Snowflake also saw solid customer growth, with net new customer additions rising 21% compared to the same period last year. Notably, customer quality is strengthening alongside quantity. During the quarter, 50 customers surpassed $1 million in trailing 12-month revenue, a record high that brings the total number of such large customers to 654. Moreover, SNOW ended Q2 with 12,062 customers.

Another encouraging indicator of future growth is the company’s remaining performance obligations (RPO), which rose 33% year-over-year to $6.9 billion. The net revenue retention rate remains robust at 125%, signaling that existing customers continue to expand their usage at healthy levels. Operational improvements are also translating to stronger profitability, with adjusted operating margins reaching 11%, up from 5% in the same period last year.

SNOW’s Upgraded Outlook Reflects Confidence

Looking ahead, Snowflake is well-positioned to deliver solid free cash flow in the coming quarters, thanks to its solid pipeline of large deals, contracted billings, and a strong base of renewals. Reflecting its confidence in demand, management raised its fiscal 2026 product revenue guidance to $4.395 billion, representing 27% growth, up from its previous projection of 25% growth.

Is Snowflake Stock a Buy Now?

Snowflake’s latest quarterly results show its ability to accelerate revenue growth, expand its customer base, and deliver stronger profitability in the face of macroeconomic uncertainty. It is capturing new demand and deepening engagement with existing clients, as reflected in its impressive net revenue retention rate and record number of high-spending customers. This combination of broad adoption and quality growth in the number of customers positions it well to deliver solid long-term growth.

With a large addressable market, a growing pipeline of high-value contracts, and improving operational leverage, Snowflake appears well-positioned to deliver sustained growth and rising free cash flow in the quarter ahead.

Analysts remain bullish on Snowflake stock, maintaining a “Strong Buy” consensus rating. While SNOW stock has gained substantially over the past year, the Street-high price target of $262 indicates a potential 31% gain from its yesterday’s closing price of $200.39.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.